Successfully navigating the Scientific Research and Experimental Development (SR&ED) tax credit program can be a significant advantage for Canadian businesses investing in innovation. However, when the Canada Revenue Agency (CRA) questions your claim, the process can become stressful and potentially costly. Knowing how to respond effectively is critical to securing your credits and avoiding delays, audits, or outright rejection. This guide explains how to handle CRA inquiries with confidence, strengthen your case with proper documentation, and protect your SR&ED benefits.

Why the CRA Questions SR&ED Claims

The CRA scrutinizes SR&ED claims to ensure businesses meet the eligibility criteria under the Income Tax Act and provide accurate documentation. Claims often get flagged for review due to:

- Insufficient project documentation or missing technical records.

- Unclear evidence of scientific or technological uncertainty in the work.

- Inflated costs or ineligible expenditures.

- Ambiguous or vague descriptions of experiments.

- Past red flags from prior audits or industry-specific scrutiny.

Understanding why your claim is under review can help you respond strategically and avoid repeating mistakes. If you’re unsure whether your project qualifies, review this guide to SR&ED eligibility to ensure your project aligns with CRA standards.

Step 1: Carefully Review the CRA’s Request

The CRA typically sends a request for information (RFI) outlining what documents, explanations, or clarifications they require. This is your opportunity to demonstrate that your project and costs meet the SR&ED criteria. Actions to take:

- Read the letter carefully – Understand whether the CRA is asking for more details, initiating a technical review, or beginning a full audit.

- Identify deadlines – The CRA often gives businesses a short window to respond. Missing deadlines can escalate the case to a formal review.

- Understand the scope – Determine if they’re questioning only project eligibility or also financial claims.

If the RFI involves a broader audit, refer to this detailed audit guide for insight into what to expect during the process.

Step 2: Organize Your Documentation

Strong, contemporaneous documentation is the cornerstone of a successful response. The CRA expects to see:

- Project plans, experiment logs, and test results proving systematic investigation.

- Evidence of technological uncertainties and advancements, such as engineering or R&D reports.

- Timesheets, payroll records, and expense tracking tied directly to eligible activities.

- Detailed descriptions of experimental processes, not just end results.

Organizing these documents early ensures you can meet CRA deadlines. Businesses often fail here, leading to rejected claims. Learn more about best practices for record-keeping in this guide on detailed SR&ED project records.

Step 3: Clarify Your Project’s Technological Uncertainty

One of the most common reasons CRA questions arise is insufficient explanation of scientific or technological uncertainty. To strengthen your case:

- Clearly state what technological barrier your team faced.

- Explain why existing solutions were insufficient or not publicly available.

- Document experiments and iterations systematically, showing the learning process.

- Emphasize that your project involved hypothesis-driven experimentation, not routine engineering.

For more detail on presenting uncertainty effectively, review how to document scientific and technological uncertainty.

Step 4: Seek Professional SR&ED Support

Responding to the CRA on your own can be risky, especially if your claim involves significant tax credits. Working with an experienced SR&ED consultant can:

- Help prepare a comprehensive response package with the right technical language.

- Negotiate with CRA reviewers to avoid unnecessary audits.

- Ensure financial calculations are airtight and meet CRA guidelines.

- Minimize the risk of claim reductions or penalties.

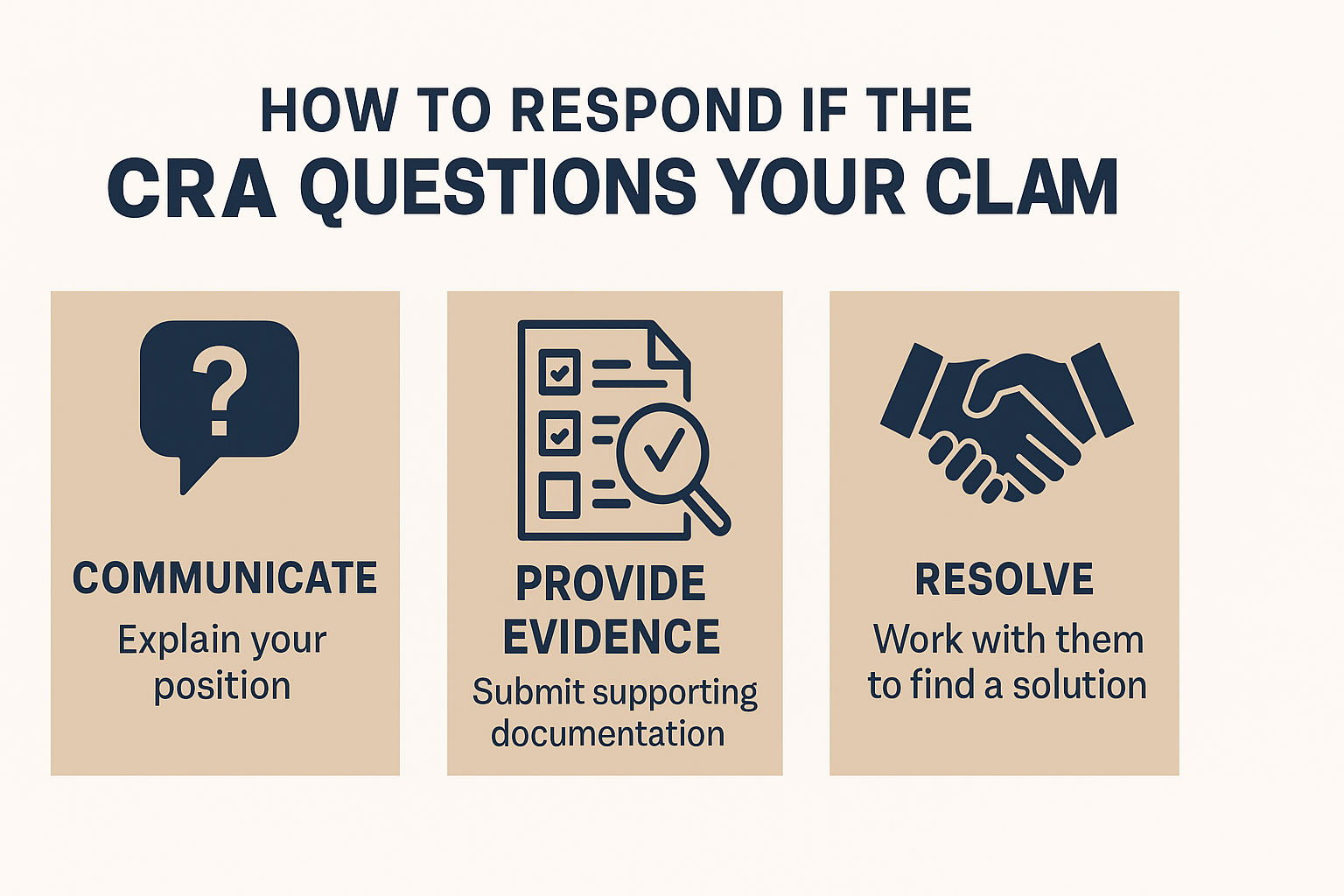

Step 5: Submit a Strong, Timely Response

When preparing your official reply:

- Be factual and concise – Avoid emotional appeals and focus on evidence.

- Organize your documents logically – Present technical reports, financial data, and supporting evidence in an easy-to-follow format.

- Address every point the CRA requested – Partial responses often trigger escalations.

- Keep copies of all submissions – These records can help in appeals if necessary.

If your company is experiencing cash flow challenges while waiting for your tax credits, consider SR&ED financing options to bridge the gap and keep projects moving forward.

What If the CRA Escalates to an Audit?

If your response doesn’t fully satisfy the CRA, they may initiate a formal SR&ED audit. This involves:

- Site visits to review R&D work and facilities.

- Interviews with technical staff to verify project claims.

- Detailed reviews of financial documentation to validate expenses.

Businesses that have prepared proactively, with clear project records and professional representation, often pass audits successfully. If you’re facing a full audit, you may also want to consult the CRA’s official SR&ED program guidelines for additional insights.

Avoiding Issues in Future Claims

To prevent future CRA challenges:

- Maintain detailed R&D logs throughout each project, not just at year-end.

- Train staff on documenting experiments and eligible work.

- Consult SR&ED experts annually to review claim strategy.

- Use tools like the SR&ED calculator to estimate and track claims accurately.

Taking proactive measures helps ensure smoother claim processing and reduces the likelihood of costly disputes.

Need Help with a CRA SR&ED Inquiry?

If your SR&ED claim is under review, professional guidance can make all the difference. Our team at SR&ED Plus Fundamentals specializes in helping businesses navigate CRA questions, audits, and financing challenges. Contact us today through our contact page to protect your claim and secure the credits your innovation deserves.